Why the Insurance Industry Isn’t Prepared for the Costly Risks of Climate Change

Alex Luna • September 7th, 2021.

We’re bringing you exclusive content from our newsletter, The Forecast, right here on Medium. Sign uphere. This story is the newsletter’s Executive Brief from ourAugust 25th, 2021, newsletter.

Drought. Floods. Freezing temperatures. Hurricanes. Wildfires. Winter storms. Every year, these weather and climate disasters claim countless lives and cause billions of dollars of damages across the world — and with climate change, they’re happening with greater severity and frequency.

So who’s paying for it? The costs fall on homeowners, business owners, federal, state, and local governments, and insurance and reinsurance companies. Increasingly, the insurance industry is caught unprepared — and liable.

Just last month, massive storms resulted in thecostliest flooding eventson record for both German and Chinese insurers. Preliminary estimates show Germany is likely to see as much as USD$20 billion in direct economic damage, and insurers face potential losses of $5.3 billion to $6.5 billion, according toAon’s monthly catastrophe report. It would be the costliest individual natural disaster for theGerman insurance industry on record. In China, meanwhile, estimates place the total economic cost of the July flooding at nearly $25 billion. The flood damage concentrated in central megacity Zhengzhou is anticipated to cost insurers up to $1.7 billion — also the highest natural disaster payout for the nation’s insurance industry on record.

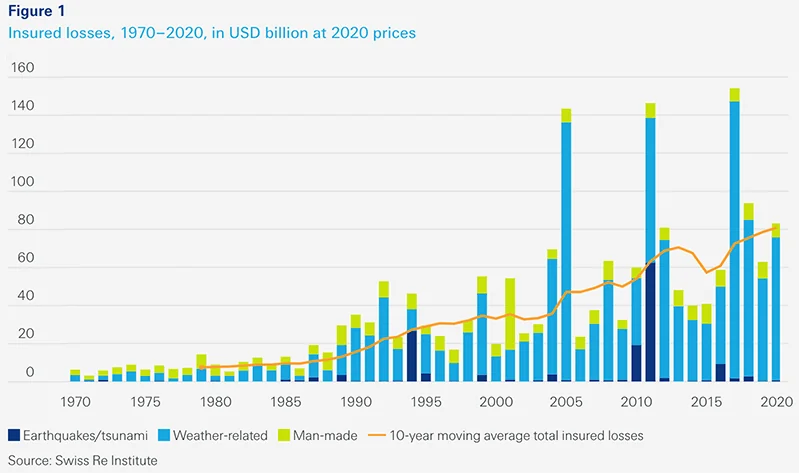

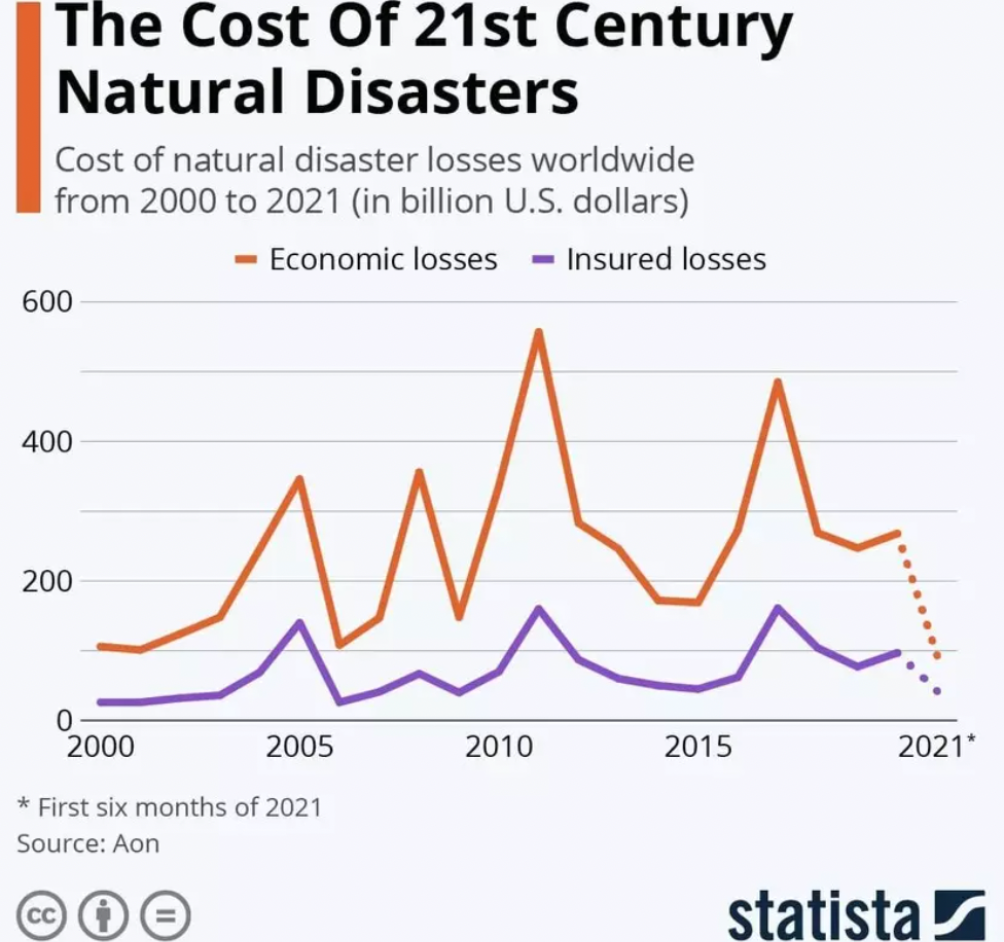

It’s part of a trend: Swiss Reinsurance Company Ltd, the world’s largest reinsurer, found that 2020 was the fifth-costliest year for the industry in 40 years. Global losses amounted to $83 billion, according to the reinsurer’s report, driven by a record number of severe storms and wildfires in the U.S. The insurance industry covered 45% of global economic losses in 2020. (Other costly years included 2005’s and 2017’s record hurricane seasons and the 2011 Japanese earthquake.)

Take property underwriting, for example. Insuring against weather and climate disasters is complex: traditional homeowners insurance covers most types of severe weather but not floods or earthquakes, which require separate policies. Those separate policies, including a common one called catastrophe insurance, come with a higher price tag. Insurers face challenges in balancing the statistical risks of disasters, the potential payouts involved, and consumer demand for policies, which rarely align. (One key is diversification: In order to be able to pay claims from thehighest-cost disasters, typically windstorms and earthquakes in the U.S., Japan and Europe, an insurer needs to do enough business elsewhere or set aside enough capital to pay for potential claims.)

However, climate change exacerbates these challenges. Insurers’models for the cost of disastersare based on historical data, but those trends are shifting in unpredictable ways as the climate warms. A warmer atmosphere, for instance, is able to carry more moisture, which means storms move slower and carry more precipitation, leading to massive and costly flooding, as seen in China and Germany last month.

Insurance companies often then turn to reinsurers — companies where insurance companies get their own insurance. Despite representingonly 5% or soof the$7 trillion in gross premiumswritten by the industry each year, reinsurers use their global reach and huge balance sheets to cover as much as two-thirds of the losses from major events.

Risk — identifying, modeling, and managing it — is core to the insurance industry. Climate change poses great long-term and increasingly short-term risk. As a result, insurers are investing significantly in building state-of-the-art climate models to better understand global warming’s impact, as well as rebalancing their premiums and pricing strategies to account for these shifts.

Indeed,Swiss Repredicted that climate-related risks would account for just over a fifth of the overall rise in property premiums over the next two decades. That’s as much as $183bn to annual premiums for property insurance by 2040.

And it is not just property and casualty insurance that’s being reevaluated. Climate change is also leaking into life insurance risk, directors and officers risk, and other areas.

If it becomes too expensive to cover losses, insurers and reinsurers will raise prices and pull back toward areas that are more profitable. Swiss Re AG, the world’s largest natural catastrophe reinsurer, said last year it had startedparing back parts of its portfoliowith high exposure to climate risks, and is raising its modeled risks associated with weather events in Australia, typhoons in Japan and wildfires in California.

That can increase the costs of coverage for primary insurers and customers down the chain — and low- or middle-income people might not be able to afford it.

The reality of the climate crisis is that no one group can afford to shoulder its costs. Insurers will have to continue to adapt their risk forecasts, premium structures, investment strategies, and claims handling practices to remain competitive in a market increasingly complicated by climate change.

Ready to find out what risk-intelligence can do for your bottom line?